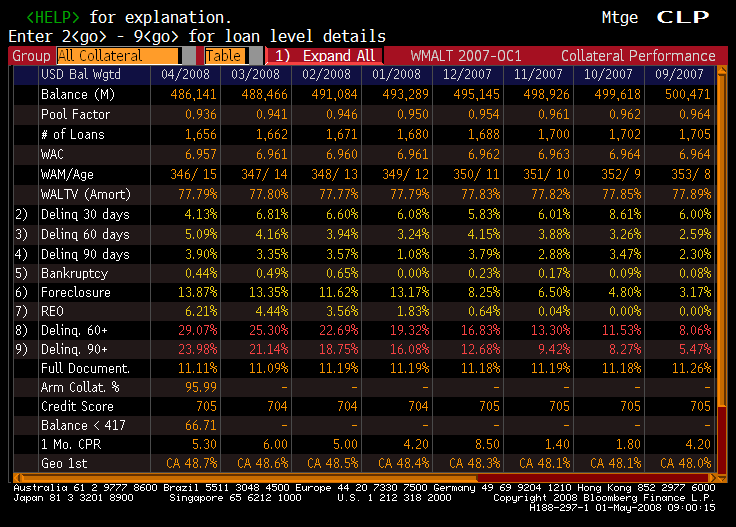

Federal Regulators shut down Washington Mutual and firesold their assets to JPMorgan Chase for $1.8 Billion. And to think Chase almost paid $8 a share earlier this year and WaMu turned them down. Hopefully none of our members are still significant debt or equity holders in WaMu.